CANADIAN MONEY MAXIMIZER app for iPhone and iPad

Developer: Nic Tustin

First release : 02 Nov 2017

App size: 8.36 Mb

IMPORTANT:

* CANADIAN MONEY MAXIMIZER will be using 2017 tax rates and 2018 TFSA contribution room from January 1, 2018 - March 31, 2018

** CANADIAN MONEY MAXIMIZER will be using 2018 tax rates and 2018 TFSA contribution room from April 1, 2018 - December 31, 2018

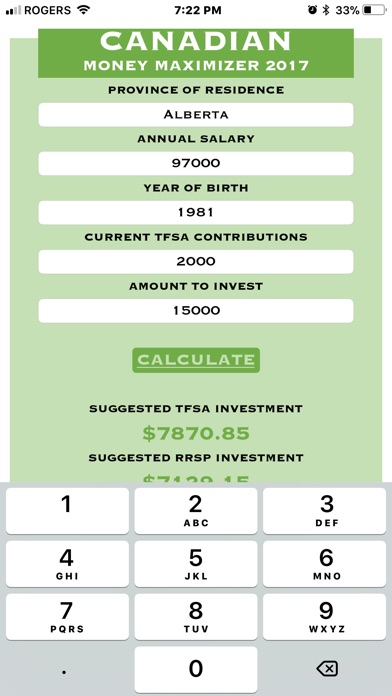

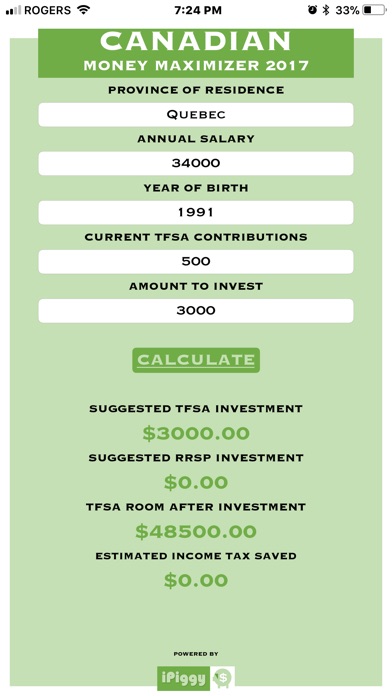

HOW IT WORKS:

Think of CANADIAN MONEY MAXIMIZER as a scientific calculator with only one specific calculation. This app truly pinpoint which distribution of income is right for each registered portfolio by accounting for the various income streams and also uses weighted tax, due to the varying provincial tax rate. When investing, it is of even importance when deciding when the money is going to be taken out as much as it is when putting money away. When taking money out of an RRSP in retirement, income is generally lower than in the work force, and in a perfect world, a lower marginal tax bracket. When taking money out of a TFSA it is especially beneficial when pulling out the funds once entering a higher tax bracket. This is because the funds are not taxed, eliminating the effect of the new marginal tax rate. On average, this creates a savings of over 6.516% for all provinces across Canada in 2017. Think of this as a "bonus" return on your investment. This being said, in general speaking, the closer an investor is to the lower end of a tax bracket, a RRSP would be more beneficial, and the closer to the upper end of a tax bracket, a TFSA would be more beneficial. CANADIAN MONEY

MAXIMIZER also takes in account an investors age. Due to contribution limits, TFSA have set maximum limits, and this app takes these values into account and shifts potential over contributed funds to the RRSP portfolio. RRSPs also have contribution limits and these are far more individualistic. Make sure that the output fits within your personal contribution room.

ABOUT:

This app will help you pay the least amount of taxes throughout your lifetime! Canada is unique in the fact that it has two different registered portfolio products which have properties that act in opposite ways. Due to the nature of these products, there is an algorithm that helps you maximize current and future income by minimizing the amount of taxes you pay. Find out if the mutual fund that youve been thinking about belongs in your TFSA (Tax Free Savings Account) and/or RRSP (Registered Retirement Savings Plan).

TFSA have specific limits depending on how old you are and each province has their own tax rate. There is a specific value tailored to where you live and the app always checks to make sure you dont over contribute to your TFSA.

Think of a TFSA as a Tax Free "Investment" Account. Securities and mutual funds can be purchased in this registered product and the best part is... no tax! Any profits gained inside a TFSA is tax free income.

If youre a millennial... TFSAs are your best friend. If youre going to collect a pension... TFSAs are your best friend. Unlike RRSPs, pulling out money in retirement from a TFSA does not affect taxable income unlike RRSPs.

TFSAs are also a great tool to build a safety net for a rainy day or an emergency fund as the funds withdrawn from the TFSA portfolio are not added to your yearly income and not taxed.

Plain and simple... RRSPSs help you reduce the income tax you pay now... but you pay tax in retirement.

Let CANADIAN MONEY MAXIMIZER find your financial "sweet spot" today!

This app takes the guess work out of your investment strategy. It calculates, to the nearest penny, how much of your investment should be contributed to a TFSA or RRSP, to truly maximize your money.